Behind the average, the fracture

The Banque de France delivered its annual financial health study of French startups in 2024. The figures confirm the solidity of an ecosystem which continues to grow despite a tense economic context. But behind the reassuring averages, the report reveals an increasing polarization: a handful of Scale-Ups draws the dynamics, while a majority remain fragile and dependent on capital.

A targeted perimeter

The study does not cover all 15,000 startups identified by the French Tech mission. The Banque de France has retained a sample of 3,930 companies corresponding to two criteria, a turnover greater than 750,000 euros or a fundraising greater than 3 million. On this group, only 2,165 had 2023 and 2024 balance sheets. In other words, the analysis does not relate to young shoots in the creation phase, but on startups already advanced in their journey.

Growth that slows down but remains superior

In 2024, French startups generated 25 billion euros in turnover, up 13 %. This pace remains sustained, even if the dynamics slow down after +18.6 % in 2023 and +25 % in 2022.

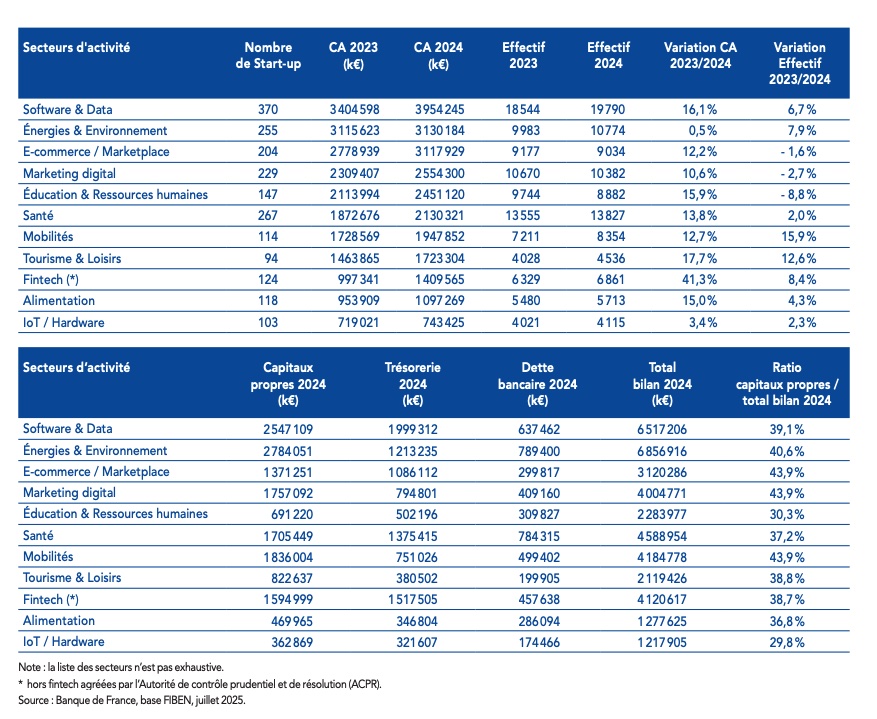

Some sectors are particularly pulling out of the game, including fintechs which increased by 41 % to reach 1.41 billion euros in income. Other structuring sectors such as software and data, energies and the environment, as well as e-commerce and marketplaces, combine almost 40 % of global turnover. Internationalization remains an essential engine: 28 % of income comes from export, or around 7 billion euros.

Profitability: the hidden side of medium -sized

The operating deficit reduced by 17 % in 2024, confirming an improvement trajectory initiated in 2022. However, 59 % of startups remain in deficit, for a total of 4.1 billion euros in losses, when 41 % generate a positive operating result of 1 billion.

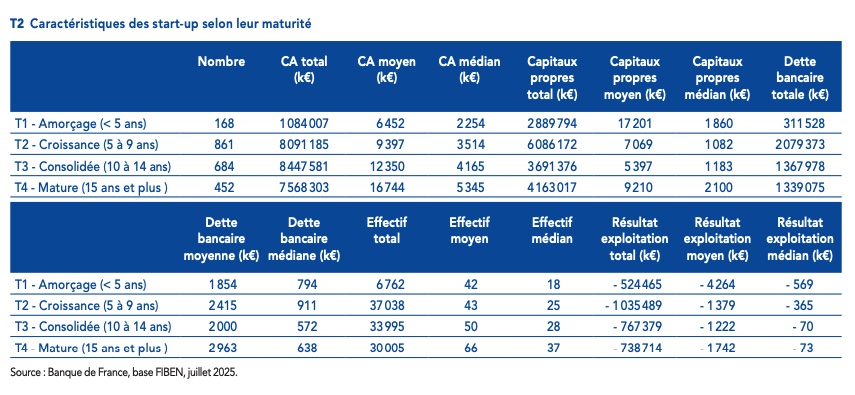

Net losses still represent 12.4 % of the cumulative turnover, compared to 16.5 % in 2023 and 21.3 % in 2022. But the average mask of large differences: among mature companies over 15 years old, the average loss reached 1.7 million euros, while the median is only 73,000 euros. This large gap is explained by a minority of surfined societies, capable of burning cash on a large scale, which draw the average down. The majority of others, with more limited resources, approach much faster from the point of balance.

Contrasting assessments

Equity increased by 18 %, to 16.8 billion euros, a sign of overall strengthening. But almost one in five startups still display negative equity, or around 380 companies.

Banking debt is gaining momentum (5.1 billion euros, used by 88 % of companies), but its weight remains contained, with a ratio debt on equity of 30 %, much lower than 66 % observed in SMEs and ETIs. Bond loans reach 1.1 billion (+23 %), often used as relays between two financing towers.

The overall cash flows at 11 billion euros, slightly increased despite the drop in levees (–7 % in 2024 according to EY). This paradox reflects an evolution of behavior, for lack of new funding, the startups have reduced their burn misses and adopted a stricter discipline to preserve their cash horizon.

The job concentrated between a few actors

The workforce increased by 4 % to reach 107,800 employees, a figure far from 1.1 million jobs claimed by French Tech for the entire ecosystem. Half of the startups employ less than 28 people, a quarter less than 14, while on the opposite, only 22 Scale-ups concentrate more than 10 % of jobs with nearly 600 employees on average.

In other words, the global dynamic of the use of FrenchTech is largely based on a small number of actors capable of recruiting massively.

Increases up

82 startups experienced a failure over a year, including 57 in 2024 and 25 in the first quarter of 2025. The 2.5 % rate remains lower than that of all French companies (3.5 to 4 %), but procedures accelerate quarter after quarter. In 70 % of cases, startups are directly placed in compulsory liquidation.

The most affected sectors are e-commerce and health. The typical profile is that of an intermediate structure: a median turnover of 3.1 million euros, around fifty employees, but insufficient equity and too low cash to absorb shocks.

Which changes compared to 2023

The comparison with the 2023 study makes it possible to better measure the evolution, we can see that the growth rate slows down: +19 % in 2023 against +13 % in 2024. Job creations are cut, going from +8 % to +4 %. On the other hand, the share of profitable startups increased, from 36 % in 2023 to 41 % in 2024, and the failure rate fell slightly, from 3.1 % to 2.5 %.

But beyond the figures, it is the context that counts, 2023 marked the brutal shock of the reversal of venture capital, with a fall of 38 % of the uprights raised. 2024 does not reflect a rebound, but continuity under duress, for lack of funding, the startups have tightened their management, reduces their burn misses and preserved their cash. This forced discipline made it possible to improve the results, without erasing the structural fracture between a few surfined scales and a majority of fragile companies.

📊 5 key lessons

- € 25 billion in turnover in 2024 (+13 %).

- € 16.8 billion in equity, but 17.5 % of negative startups.

- € 11 billion in preserved cash flow despite the drop in levees.

- 107,800 employees, but the employment concentrated on a few scale-ups.

- 82 failures in one year, or 2.5 % of the panel.

Between continuity and uncertainty

In 2024, French Tech showed that it could grow while reducing its losses. But the ecosystem remains fractured between an elite of well-funded, already internationalized and sometimes profitable Scale-Ups, which concentrates most of the dynamics and the opposite, a majority of startups, often undercapitalized, still survive thanks to the flow of private and public capital.

The year 2025 opened on a more uncertain climate. If the public devices (France 2030, Tibi 2, French Tech 2030) continue to play their role as shock absorber, the growing prudence of investors, combined with political tensions and the opposite of the global economy, could accentuate natural selection. Some startups will finally cross the profitability threshold for forced march, while others, for lack of critical size, will be absorbed or disappeared.